Brochure/leaflet

UoDSS newsletter 2025

2025 newsletter from your Trustee Chair

Updated on 12 May 2025

Letter from the Chair of Trustees

Dear Member,

Welcome to the fifth edition of our Trustee Newsletter which we hope you will find interesting and informative.

We are pleased to report that the Scheme’s funding shortfall has reduced during the last Scheme year. The main reason for the improvement is due to a better than expected return on the Scheme’s assets, the past deficit repair contributions which are being paid by the University to the Scheme and the contribution towards future benefits which are being paid by the Employee members and the University.

More details on the Scheme’s funding position (including information we are obliged to include as a result of current legislation) is included in the Scheme’s Summary Funding Statement in this edition of the Newsletter.

Future Benefit Provision from 1 September 2024

Following further consultation during August 2024, the University has decided to increase the amount of pension built up in future for existing members from 1/100th to 1/80th. A cash sum of three times the pension will also be provided on retirement (you may recall that previously, benefits building up after 1st January 2023 had been reduced from 1/80th to 1/100th but this has been reversed back with effect from 1st September 2024).

Employee contributions decreased from 8.75% to 5.74% of earnings. These changes took effect from 1st September 2024 and there is no change to benefits built up before this date. It is important to note that the Scheme Trustee looks after the benefits promised and cannot influence employment contract terms.

My Pocket Pensions

As you will see later in the newsletter, we have included some information about the My Pocket Pensions app which allows members to access their Scheme pensions information more easily and quickly. We recommend using this app for that reason and you can find more details about the app in this newsletter.

Current Issues

We have included a number of articles on current pensions issues that we hope will be of interest to you. These are:

- Upcoming changes to the minimum age at which you can access your pension benefits;

- Details of how you can obtain information on your State Pension; and

- Details of changes to the UK’s pension taxation rules

We welcome any questions or feedback you have, either on this newsletter or any aspect of the Scheme. Please do let us have your views on this newsletter using the contact details.

Yours faithfully

Keith Swinley

Chair of the Trustees of the University of Dundee Superannuation and Life Assurance Scheme April 2025

Changes to the Trustee Board

Since our last Newsletter, there have been some changes to the Trustee Board. Shona Johnston has stood down after 5 years as an Employer Nominated Trustee Director. I would like to take this opportunity on behalf of the Trustee Directors to thank Shona for her service to the Scheme.

Joining the Trustee Board are Louise Stanley as an Employer Nominated Trustee Director and David Ritchie as a Member Nominated Trustee Director.

Your Trustees and Advisers

The Scheme is managed by its Trustee, a company called the University of Dundee Superannuation Scheme Trustees Limited. This company currently has nine directors. Four directors are nominated by the University of Dundee and four are elected by Scheme members and one being an independent professional Trustee Director.

Current directors

Employer nominated:

- Keith Swinley (Chair of Trustee)

- Martin Glover

- Richard Parsons

- Louise Stanley

Member nominated:

- Peter Hewitt

- David Ritchie

- James Rourke

- Fiona Woodward

Independent:

- Allan Martin

Current advisors

- Alan Collins - Scheme Actuary

- Pinsent Masons LLP - Legal Advisers

- Spence & Partners - Administrators, Actuarial and Investment Advisers

- BDO LLP - Independent Auditor

Investment Managers

- Aberdeen Standard Investments Limited - (Transfer agent:Brown Brothers Harriman)

- Partners Group (UK) Ltd

- Legal &General Investment Management Limited

Investment Update

Towards the end of 2023 lower inflation numbers and weaker economic data caused central banks to take a more dovish stance with rate cuts being priced in for 2024 which led most asset classes to rally significantly. The rally continued into Q1 2024 and was mostly concentrated in equities with Global Equities whilst Global Bonds and Real Estate generated negative returns during the period.

Resilient economic data coming out of the US was supportive of equity markets more broadly, however the news caused the Federal Reserve to reverse it’s more dovish tone which in turn weighted on bond valuations and other interest rate sensitive assets such as Real Estate.

The increase in inflation at the start of 2024 caused many central banks to reverse their previous stance, as it became clear they hadn’t achieved their aim of reducing inflation via their interest rate hiking cycle.

The strong momentum witnessed by equity markets in the first quarter of 2024 carried on into the second quarter as continued robust economic growth was positive for growth assets. However, this did lead to a continuation of the higher for longer interest rate narrative that consequently weighed on Global Bond and Real Estate valuations.

Within Equities, Asia Ex Japan was one of the strongest performing regions followed closely by Emerging Markets (EM) The Chinese government’s decision to support the real estate sector was positive for Chinese equities as well as EM more broadly. The strength of the Chinese market coupled with the strong performance of A.I companies exposed to the Taiwanese stock market helped Asia Ex Japan deliver strong returns. US equity markets also performed strongly mainly driven by US technology companies. Positive gains across other European markets were offset by weakness in the French Equity market in June, as uncertainty around the outcome of the snap French Federal election weighed on market sentiment. Conversely, the Japanese Stock Market posted a negative return in GBP terms, despite generating some strong returns in Q1-24. The main driver of this negative performance was the continued depreciation of the Yen against the pound due to the Bank of Japan’s (BoJ) decision to end 8 years of negative rates.

Commodities continued their positive momentum into the second quarter mainly driven by a rally in industrial and precious metals off the back of continued robust economic growth.

Higher inflation numbers and better economic data weighed on the more interest-rate sensitive investment grade bonds.

Following the Scheme year-end most asset classes delivered strong returns as the start of the US Federal Reserve’s (“Fed”) rate cutting cycle was welcomed by investors as an indication that it had achieved its aim of combatting the elevated levels of inflation. As a result, Global listed Real Estate delivered the highest returns with Global Bonds also delivering strong returns as the prospect of lower rates going forward was positive for valuations. However, the quarter was still punctuated by a bout of market volatility when weak US economic data and an interest rate hike by the Bank of Japan (“BOJ”) caused markets to sell-off in early August.

Summary Funding Statement Funding

Update as at 31 July 2024

As a member of the University of Dundee Superannuation & Life Assurance Scheme (“the Scheme”) you are entitled to receive an update of the Scheme’s funding level. Legislation requires that this information is made available to all Scheme members following completion of each Actuarial Valuation or following each Annual Funding Update.

No action is needed from you. This statement is for your information only and is provided to help you understand the way in which the Scheme’s financial position is assessed. Should you wish to obtain more information or copies of the Scheme documents, you can contact us and we will be pleased to assist. Contact details are given at the end of this statement.

How does the Scheme operate?

The Scheme provides for a lifetime annual pension in retirement and a one off lump sum at retirement, along with dependant benefits on death.

The University of Dundee and the Dundee University Students’ Association (“the Employers”) contribute to the Scheme, and their contributions together with any contributions the members made are invested.

These contributions together with the investment returns are used to pay for members’ benefits. This money is held in a common fund, which means that there are no separate funds for each individual.

How is the financial security of the Scheme assessed?

An in-depth assessment of the Scheme’s financial situation is carried out at least every three years in a process known as an Actuarial Valuation. The most recent Actuarial Valuation was carried out as at 31 July 2023. The Actuarial Valuation is carried out by a qualified, independent professional known as the Scheme Actuary.

The Scheme Actuary also carries out annual checks on the financial security of the Scheme between full Actuarial Valuations, known as Annual Funding Updates. The results of these checks are shown in the Actuarial Report for the Scheme. The most recent Annual Funding Update was carried out as at 31 June 2024, and the results of that update are also shown in this statement. The results of the Annual Funding Update as at 31 July 2023 are also shown for comparative purposes.

The approach adopted for the Actuarial Valuation is agreed with the Employers and is set out in a document known as the Statement of Funding Principles (“the SFP”).

The purpose of the Actuarial Valuation is to compare the Scheme’s liabilities to the Scheme’s assets on an ongoing basis.

- If the value of the assets is less than the value of the liabilities, the Scheme is said to have a “shortfall”.

- If the value of the assets is more than the value of the liabilities, the Scheme is said to have a “surplus”.

The Scheme’s funding level is expressed as the percentage of the Scheme’s assets relative to the value of the Scheme’s liabilities.

The Actuarial Valuation also compares the Scheme’s liabilities on a solvency basis to the value of the Scheme’s assets.

The main purpose of the Annual Funding Update is to show an approximate update on the progress of the Scheme’s ongoing funding level since the Actuarial Valuation.

Jargon Buster

- Scheme liabilities are the estimated cost of providing benefits for all members included in the Scheme.

- Scheme assets are the funds built up from monies invested, together with returns on the Scheme’s investments.

- The Ongoing basis for an Actuarial Valuation assumes that the Scheme will continue in the future and has no plans to wind up.

- The Solvency basis for an Actuarial Valuation estimates the amount needed to fully secure all benefits built up to date from an insurance company if the Employers decided to wind up the Scheme.

Ongoing Funding Position

An Annual Funding Update was carried out as at 31 July 2024 and the results of this update together with the results of the Actuarial Valuation as at 31 July 2023 and the previous update as at 31 July 2022 are shown below.

| Description | 31 JULY 2022 (£m) | 31 JULY 2023 (£m) | 31 JULY 2024 (£m) |

|---|---|---|---|

| Scheme liabilities | 165.3 | 122.2 | 123.1 |

| Scheme assets | 120.5 | 95.3 | 106.7 |

| Shortfall | 44.8 | 26.9 | 16.5 |

| Funding level | 73% | 78% | 87% |

Change in Funding Level Since the Annual Funding

Update as at 31 July 2022

The funding level of the Scheme has significantly improved since the last funding update as at 31 July 2022. The main reasons for the improvements are deficit payments made by the Employers and rising interest rates placing a lower value on the Scheme’s liabilities. These improvements have been offset in part by a reduction in the value of the Scheme’s assets (resulting mainly from bond assets falling in value due to higher interest rates).

The Trustee and the Employers will continue to monitor the funding level on a regular basis in order to ensure that the Scheme’s funding remains on track over the long-term.

Eliminating the Shortfall

The Actuarial Valuation as at 31 July 2023 showed a shortfall and so a recovery plan was agreed to eliminate the shortfall with deficit reduction contributions of around £3.7m a year.

Based on the agreed Recovery Plan, the Trustees estimate that the shortfall will be cleared by 31 July 2029.

The Employers also make contributions towards the cost of future benefits and the costs of administering the Scheme including the payment of levies.

Details of the contributions payable into the Scheme and details of how expenses are paid is contained in a document called the Schedule of Contributions. We can provide a copy if requested.

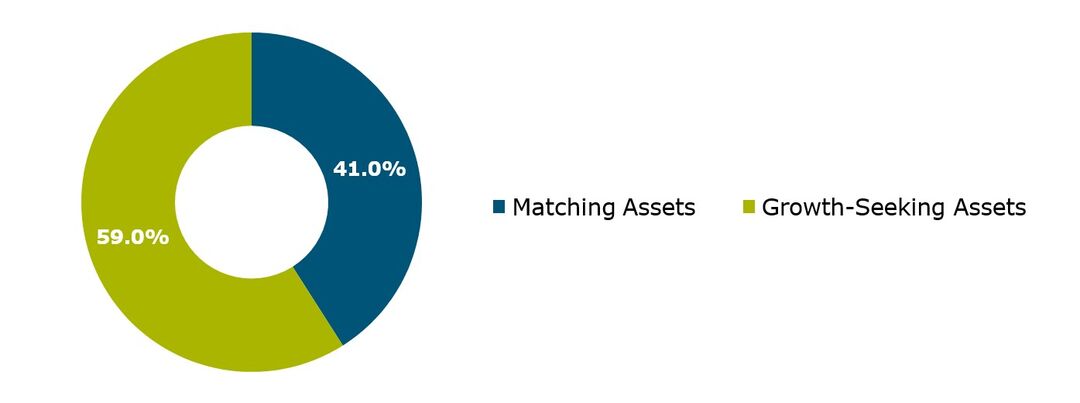

How are the Scheme’s assets invested?

The Trustee’s policy is to invest in a wide range of assets. The Scheme’s asset allocation as at 31 July 2024 is shown in the diagram below.

The most recent Statement of Investment Principles (“SIP”) was agreed in September 2024. The SIP sets out the principles governing decisions about how the Scheme’s assets are invested. The actual allocation of assets held at a particular time may differ from the strategic allocation within acceptable limits. Read the latest SIP

The Scheme’s asset value includes the Scheme’s invested assets and net current assets.

Asset Distribution

Financial support for the Scheme

The Trustee’s objective is to have enough money in the Scheme to pay pensions now and in the future. However, the Scheme relies on the Employers continuing to support it because:

- The funding level can fluctuate, and when there is a funding shortfall, the Employers will usually need to put in more money; and

- The target funding level may turn out not to be enough so the Employers will need to put in more money.

What would happen if the Scheme had to wind up?

Although the Scheme is not in the process of winding up, we are required by legislation to advise you what would happen in these circumstances. If the Scheme had started winding up as at 31 July 2023, the additional assets needed to secure full member benefits with an insurance company would have been approximately £55.4m.

Inclusion of this information does not imply that the Employers are thinking of winding up the Scheme.

If the Scheme were to wind up, the Employers would need to pay sufficient money into the Scheme to enable members’ benefits to be secured by an insurance company.

If the Scheme were to wind up and the Employers could not afford to pay the full amount, you might not receive your full benefit entitlement, even if the Scheme is fully funded on the approach set out in the Statement of Funding Principles.

If the Employers became insolvent, the Pension Protection Fund (“PPF”) might be able to take over the Scheme and pay compensation to members.

Further information and guidance can be obtained from the PPF’s website. You can also write to the PPF at Renaissance, 12 Dingwall Road, Croydon, Surrey, CR0 2NA.

Why does the funding Scheme not call for full solvency at all times?

The full solvency position assumes that benefits will be secured by buying insurance policies. Insurers are obliged to take a very cautious view of the future and need to make a profit. The cost of securing pensions in this way also incorporates the future expenses involved in administration. By contrast, our funding Scheme assumes that the Employers will continue in business and continue to support the Scheme.

Payment from the Scheme

The Trustee is required to confirm to you whether there have been any payments to the Employers out of the Scheme’s assets in the previous 12 months. There have been no such payments.

Changes to the Scheme

The Trustee is also required to confirm to you that the Pensions Regulator has not given any directions in relation to the funding of the Scheme or imposed a Schedule of Contributions on the Scheme. There have been no such impositions.

Internal Dispute Resolution Procedure

In the event that you have a complaint, you should first raise this with the Trustee through the Scheme’s Internal Dispute Resolution Procedure (“IDRP”).

A copy of the IDRP can be obtained by contacting the Trustee.

How we look after your data

The Trustee hold your personal data in order to effectively administer the Scheme. The Trustee has a legitimate interest to hold your personal data to:

- pay the correct benefits to you and your beneficiaries, if applicable;

- ensure that the Scheme is appropriately funded;

- ensure that you can receive information and updates about the Scheme, where necessary; and

- ensure that the Scheme is administered in accordance with all applicable laws.

The Trustee will only use your personal data for the purposes for which they collected it, unless they reasonably consider that they need to use it for another reason and that reason is compatible with the original purpose.

The security of your data is of paramount importance to the Trustee and the Scheme’s administrators, Spence. Spence continues to be certified and independently audited under the International Organisation for ISO 27001, an internationally recognised standard for information security management. Spence is also certified and audited in accordance with the Cyber Essentials plus scheme.

Further information on the measures taken to protect your data and your rights as a data subject can be obtained from the Trustee’s data protection representative who can be contacted at [email protected]

A list of more detailed documents which provide further information is included below and if you would like to view any of these documents, please let us know.

- Statement of Funding Principles sets out the Scheme’s funding plan.

- Recovery Plan explains how the funding shortfall is being made up.

- Schedule of Contributions shows how much money is being paid into the Scheme.

- Statement of Investment Principles explains how the Trustee invests the Scheme’s assets.

- Implementation Statement considers whether these investment principles have been followed by the Scheme’s investment managers.

- Both Statement of Investment Principles and Implementation Statement can be found at UoDSS Statement of Investment Principles (SIP)

- Annual Report and Accounts of the Scheme shows the Scheme’s income and expenditure and is prepared for each Scheme year ending 31 July. The most recent available is for the year ending 31 July 2024.

- Actuarial Valuation Report following the Scheme Actuary’s review of the Scheme’s funding position as at 31 July 2023.

- Actuarial Report the Annual Funding Updates on the Scheme’s funding position as at 31 July each year, the most recent being as at 31 July 2024.

- Scheme Booklet you should have been given a copy of this when you joined the Scheme.

Pension News

How to Access Information on your State Benefits

The State Pension - Background

A new State Pension (nSP) was introduced from 6 April 2016 for people reaching State Pension age (SPA) from that date. People who had already reached SPA continue to get their pension under the ‘old rules’.

The nSP is different in several ways:

- The full rate is set above the basic means-tested guarantee in Pension Credit

- People with no National Insurance (NI) record before April 2016 need 35 qualifying years for the full amount. (Transitional arrangements mean that not everyone with 35 qualifying years in April 2016 will receive this amount)

- It is single-tier, so the option to ‘contract-out’ has ended

The ability to derive an entitlement based on the NI record of a former spouse or civil partner has been removed, with limited transitional protection.

The full State Pension is currently £221.20 per week. Once in payment, the nSP increases at least in line with earnings, although in recent years governments have made a commitment over and above this to uprate it by the ‘triple lock’ – the highest of earnings, prices or 2.5%.

How do I know what my State Pension will be

You can ask for a forecast of your State Pension on the Gov.uk website.

In order to access the service, you will need a Government Gateway ID (if you don’t already have one).

The rules associated with the State Pension are explained in more detail in a Department for Work and Pensions leaflet entitled “Your State Pension Explained”.

Increase to the Normal Minimum Pension Age

The Normal Minimum Pension Age (“NMPA”) is the minimum age at which most pension scheme members can access their pension without incurring an unauthorised payments tax charge. Some members may be exempt, for example those retiring due to ill health.

The current NMPA is set by the Government as age 55. However, the Government has confirmed plans to increase this to age 57 from 6 April 2028, alongside planned increases in the State Pension Age (“SPA”) to 67. From then on, the current government’s intention is that the NMPA will remain ten years below the SPA. The SPA has been increasing since December 2018. Anyone born between 6 October 1954 and 5 April 1960 will reach their SPA on their 66th birthday. Anyone born after 5 April 1960 will have an SPA of 66 and one month or higher. The Government has already increased the SPA to 68 from 2046 but is planning to bring the date at which the SPA reaches 68 forward. You can confirm your State Pension Age and obtain a forecast of your State Pension on the Gov.uk website.

This change will not affect your ability to take your Scheme pension at earlier ages due to ill health, or if you qualify for an earlier protected pension age.

Abolition of the Lifetime Allowance (LTA)

The LTA was the maximum amount of tax relievable pension savings an individual could benefit from over the course of their lifetime. Pensions with value in excess of the lifetime allowance were subject to additional tax.

In 2023, the government announced that it would abolish the LTA and this has now been replaced with two new allowances:

- The Lump Sum Allowance (LSA) which limits the cumulative amount of PCLS and the tax-free element of an Uncrystallised funds pension lump sums (UFPLS) which can be paid to a member from registered pension schemes. The LSA is fixed at £268,275 (25% of the LTA at the point of abolition).

- The Lump Sum & Death Benefit Allowance (LS&DBA) which limits the cumulative amount of the tax-free element of authorised lump sums and lump sum death benefits which may be paid to or in respect of a member from registered pension schemes. The LS&DBA is fixed at £1,073,100 (the standard LTA at the point of abolition).

Following the abolition of the LTA, regular pension income will not be subject to the additional taxation (i.e. only income tax is applied). For most lump sums and lump sum death benefits, a limit remains on how much can be paid tax free by pension schemes (with income tax payable on benefits above the tax-free limits).

Inheritance Tax

On the 30 October 2024, Rachel Reeves delivered her budget statement and spoke about the government wanting to fill “the £22bn “black hole”” in the public finances left behind by the previous government whilst complying with its manifesto promise of not raising income tax.

The most significant tax change for pensions that was introduced is that from 6 April 2027, “most unused pension funds and death benefits” i.e. almost all pension benefits that pass on death will be included in a person’s estate for Inheritance Tax purposes. The Government estimates it will raise £1.46bn a year by April 2030.

The Trustee are considering any potential implications for members of the Scheme and will provide further information on this topic later in 2025.

Protecting you against pension scams

It is exceptionally important that you stay alert to the danger of scams. The Scheme’s administrator has measures in place to combat pension scams – but it still could be you! Market volatility and economic uncertainty often present opportunities for people running scams, and the Trustee will remain vigilant and follow best practice in this area. This means we might ask you additional questions if you are looking to transfer your benefits out of the Scheme and ultimately the Trustee may refuse to complete the transfer if there is evidence that you are at a risk of being scammed.

We also encourage you to be on the lookout for pension scams. Follow these four simple steps to protect your pension savings:

- Say no to unexpected pension offers – cold calling is illegal and you should be wary. An offer of a free pension review from a firm you have not used before may be a scam.

- Check who you are dealing with – Make sure anyone offering you advice is authorised to give pensions advice by calling the Financial Conduct Authority (FCA) Consumer helpline on 0800 111 6768. If you do not use an FCA-authorised firm, you may not have access to compensation schemes. A list of FCA-regulated, qualified financial advisers can be found at the Unbiased website.

- Do not be rushed or pressured – Take your time and make all the checks you need, even if this means turning down an ‘amazing deal’.

- Get impartial information or advice – You should seriously consider taking independent financial advice before changing your retirement benefits. In some cases, you may be required to do so.

If you are unsure about any approach, please do not hesitate to contact Spence to discuss. There is also help available via the Financial Conduct Authority website; and Action Fraud on 0300 123 2040.

My Pocket Pensions – a simple way to manage your Scheme pension

My Pocket Pensions is a phone app that allows you to:

- View your pension and cash lump sum from age 55-75 (for active and deferred members only);

- Get an estimate of your transfer value, updated daily;

- Understand what happens to your pension when you die;

- Let us know about any changes to your personal circumstances;

The app uses a simple registration process with a personalised QR code and it typically takes less than a minute to register for the app. Even if you want to check the Scheme’s rules at any point these are embedded within the app together with a virtual library of key Scheme documents. It allows you to use SMS messaging to and from the administrator and members can easily keep personal details up to date.

We would recommend using the app to access your pensions information more easily and quickly any time of the day. Please contact [email protected] for further details on how to register.

Summary from the latest Scheme accounts

Below is a summary of the latest audited Scheme report and accounts for the year to 31 July 2024. The full annual report has been audited by BDO LLP and a copy is available on request. Totals may not sum due to rounding.

| All figures are in £000 Income | Amount |

|---|---|

| University contributions (accrual, including employee salary sacrifice) | 7,074 |

| University contributions (deficit recovery, regular) | 3,713 |

| University contributions (special, one-off deficit recovery) | - |

| Employee contributions | 87 |

| Other income | 385 |

| Total | 11,259 |

| Outgoings | |

| Retirement and death benefits | (5,299) |

| Payments to and on account of leavers | (63) |

| Administration expenses | (490) |

| Total | (5,852) |

| Income less Outgoings | 5,407 |

| Snapshot | |

| Value of the Scheme’s assets at 31 July2023 | 95,325 |

| Incomes less Outgoings | 5,407 |

| Increase in market value of the Scheme’s investments | 6,624 |

| Value of the Scheme’s assets at 31 July2024 | 107,356 |

At 31 July 2024, there were 2,362 members of the Scheme of whom 769 were active, 924 were deferred members, and 669 were pensioners.

If you want more information about your benefits, please contact the administration team as follows:

The Trustee of the University of Dundee Superannuation and Life Assurance Scheme c/o Spence & Partners Ltd.

The Culzean Building

36 Renfield Street

Glasgow

G2 1LU

- Telephone: 0141 331 9974

- Email: [email protected]